Weaker crude prices and refining margins are likely forcing four of the five supermajor oil companies to borrow money to fund $15 billion in share buybacks for the most recent quarter, raising doubts over the payouts’ long-term sustainability.

Exxon Mobil Corp., Chevron Corp., Shell Plc, TotalEnergies SE and BP Plc are expected to post a 12% dip in earnings from last quarter to a combined $24.4 billion when they report results this week, according to the average of analysts’ estimates compiled by Bloomberg. That will leave them all — except Shell — unable to cover their dividends and buybacks with free cash flow, which is expected to be 30% lower than a year ago.

Share buybacks have become a cornerstone of Big Oil’s strategy as the post-Covid commodities rally spurred record profits and provided an opportunity to court investors betting against a fast energy transition. But with cash flow declining, those shareholder return pledges are now under strain. Crude prices are down about 17% from this year’s high even as tensions escalate in the Middle East. Third-quarter profits will be half the level of their record highs in 2022 and the lowest since 2021.

“The scales are tilting more bearish for oil prices as we look ahead,” said Noah Barrett, Denver-based lead energy research analyst at Janus Henderson, which manages about $361 billion. “They’ll likely have to lean on the balance sheet if they want to maintain the current pace of buybacks.”

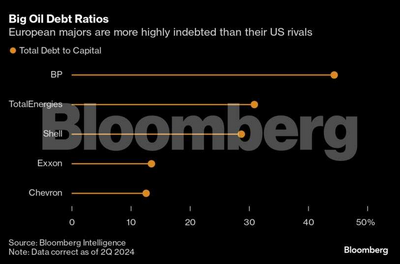

Exxon and Chevron have debt-to-capital ratios below 15% according to data compiled by Bloomberg, well below their medium-term target range of 20% to 25%. That gives them plenty of room to borrow to fund buybacks.

The European majors have higher debt levels, allowing less room to maneuver. BP warned of rising net debt levels earlier this month despite already having the highest leverage ratio among its peers. The company is also the worst performing Big Oil stock this year, declining 13% compared with a 2.3% drop in crude.

Borrowing to buy back shares isn’t uncommon in the oil business. It can boost equity returns when stock valuations are low, avoiding the cyclical buyback trap of only purchasing shares when prices are high. But a dimming outlook for oil prices next year means the cash shortfall is apt to continue over the longer term.

Borrowing to buy back shares isn’t uncommon in the oil business. It can boost equity returns when stock valuations are low, avoiding the cyclical buyback trap of only purchasing shares when prices are high. But a dimming outlook for oil prices next year means the cash shortfall is apt to continue over the longer term.

OPEC recently cut its global oil demand forecast for the third time in as many months in part due to China’s economic slowdown. Despite its worsening outlook, the cartel plans to begin boosting supplies by 2.2 million barrels a day in monthly increments starting in December. Meanwhile, non-OPEC production growth is strong, particularly in the Americas. The US, Guyana, Canada and Brazil are on course to add nearly 1 million barrels a day in 2025, Barrett said.

Borrowing to fund buybacks “could be a good use of cash while companies have reasonably strong balance sheets,” Kim Fustier, head of European oil and gas equity research at HSBC Plc, said in an interview. “The question is, ‘how sustainable will it be?’”

Refining, which often helps keep earnings steady when oil prices drop, is also under pressure. Exxon, TotalEnergies, BP and Shell have all warned of falling margins at their fuel-making divisions globally in the third quarter, as demand for fossil fuels wanes and supply grows.

“Refining’s platinum age” is coming to an end as profit margins have “steadily eroded” since their record highs in 2022, analysts at Bank of America Corp. wrote in a note this month. The worst may be yet to come. Global refining capacity will rise by 730,000 barrels a day in 2025 and by 660,000 barrels a day in 2026 as expansions in Mexico, the Middle East and China offset closures in the US and Europe, BofA said.

Exxon is the best performer among the supermajors this year, having climbed 20% while adding $130 billion to its market capitalization. That’s more than the entire value of BP. Investors will be watching to see whether it can maintain strong production growth in Guyana, where it controls an 11-billion barrel discovery, and in the US Permian Basin, where it recently expanded with the $60 billion acquisition of Pioneer Natural Resources Co. Both projects deliver crude for less than $35 a barrel.

Exxon is the best performer among the supermajors this year, having climbed 20% while adding $130 billion to its market capitalization. That’s more than the entire value of BP. Investors will be watching to see whether it can maintain strong production growth in Guyana, where it controls an 11-billion barrel discovery, and in the US Permian Basin, where it recently expanded with the $60 billion acquisition of Pioneer Natural Resources Co. Both projects deliver crude for less than $35 a barrel.

Chevron’s stock has trailed its US rival this year after its $53 billion deal to buy Hess Corp. stalled due to an arbitration battle with Exxon. Chief Executive Officer Mike Wirth will be keen to show its delayed and overbudget Tengiz project in Kazakhstan is on track for completion next year and provide an update on its Israeli gas operations, which have lost production time due to the ongoing conflict with Iran and its allies.

Investors will also be watching for the “continued normalization” of trading earnings, according to HSBC’s Fustier. It could become a “material headwind” for BP and Shell, which have historically derived large profits from the business, she said.

Exxon Mobil Corp., Chevron Corp., Shell Plc, TotalEnergies SE and BP Plc are expected to post a 12% dip in earnings from last quarter to a combined $24.4 billion when they report results this week, according to the average of analysts’ estimates compiled by Bloomberg. That will leave them all — except Shell — unable to cover their dividends and buybacks with free cash flow, which is expected to be 30% lower than a year ago.

Share buybacks have become a cornerstone of Big Oil’s strategy as the post-Covid commodities rally spurred record profits and provided an opportunity to court investors betting against a fast energy transition. But with cash flow declining, those shareholder return pledges are now under strain. Crude prices are down about 17% from this year’s high even as tensions escalate in the Middle East. Third-quarter profits will be half the level of their record highs in 2022 and the lowest since 2021.

“The scales are tilting more bearish for oil prices as we look ahead,” said Noah Barrett, Denver-based lead energy research analyst at Janus Henderson, which manages about $361 billion. “They’ll likely have to lean on the balance sheet if they want to maintain the current pace of buybacks.”

Exxon and Chevron have debt-to-capital ratios below 15% according to data compiled by Bloomberg, well below their medium-term target range of 20% to 25%. That gives them plenty of room to borrow to fund buybacks.

The European majors have higher debt levels, allowing less room to maneuver. BP warned of rising net debt levels earlier this month despite already having the highest leverage ratio among its peers. The company is also the worst performing Big Oil stock this year, declining 13% compared with a 2.3% drop in crude.

OPEC recently cut its global oil demand forecast for the third time in as many months in part due to China’s economic slowdown. Despite its worsening outlook, the cartel plans to begin boosting supplies by 2.2 million barrels a day in monthly increments starting in December. Meanwhile, non-OPEC production growth is strong, particularly in the Americas. The US, Guyana, Canada and Brazil are on course to add nearly 1 million barrels a day in 2025, Barrett said.

Borrowing to fund buybacks “could be a good use of cash while companies have reasonably strong balance sheets,” Kim Fustier, head of European oil and gas equity research at HSBC Plc, said in an interview. “The question is, ‘how sustainable will it be?’”

Refining, which often helps keep earnings steady when oil prices drop, is also under pressure. Exxon, TotalEnergies, BP and Shell have all warned of falling margins at their fuel-making divisions globally in the third quarter, as demand for fossil fuels wanes and supply grows.

“Refining’s platinum age” is coming to an end as profit margins have “steadily eroded” since their record highs in 2022, analysts at Bank of America Corp. wrote in a note this month. The worst may be yet to come. Global refining capacity will rise by 730,000 barrels a day in 2025 and by 660,000 barrels a day in 2026 as expansions in Mexico, the Middle East and China offset closures in the US and Europe, BofA said.

Chevron’s stock has trailed its US rival this year after its $53 billion deal to buy Hess Corp. stalled due to an arbitration battle with Exxon. Chief Executive Officer Mike Wirth will be keen to show its delayed and overbudget Tengiz project in Kazakhstan is on track for completion next year and provide an update on its Israeli gas operations, which have lost production time due to the ongoing conflict with Iran and its allies.

Investors will also be watching for the “continued normalization” of trading earnings, according to HSBC’s Fustier. It could become a “material headwind” for BP and Shell, which have historically derived large profits from the business, she said.

You may also like

NATO, Russia edge closer to standoff over airspace incursions

ED dispatches key officers to Mauritius to provide specialised training to FCC

Drivers could be fined £5,000 for splashing pedestrians in the rain

Pension credit claimants must tell DWP of 10 changes or risk losing it- full list

Over 60 flights cancelled, 42 others delayed at Kolkata airport following heavy rain overnight